Phone Stolen No Insurance? Here’s What Happens Next

Picture this: you set your phone down at a coffee shop for just a moment, and when you reach for it — it’s gone. Your stomach drops. Then comes the next gut punch: you never got phone insurance.

If you’re dealing with a phone stolen no insurance situation right now, you’re not alone — and you’re not completely out of options either. This guide walks you through exactly what happens, what you can do, and how to avoid this nightmare in the future.

What Happens When Your Phone Gets Stolen and You Have No Insurance?

When your phone is stolen and you have no insurance policy in place, you typically bear the full financial cost of replacing it. Depending on your device, that could mean paying anywhere from $200 to over $1,200 out of pocket for a replacement — with no guaranteed reimbursement from any source.

Beyond the financial hit, you may also face risks like unauthorized account access, identity theft, and data loss. The situation is serious, but there are still some paths forward worth exploring.

Short Answer: Are You Covered Without Phone Insurance?

In most cases, no. If you have no dedicated phone insurance or protection plan, you are generally responsible for replacing the device entirely at your own expense.

However, depending on your circumstances, you may have partial or indirect coverage through other sources — such as your credit card, homeowners insurance, or carrier warranty program. It depends entirely on your existing policies.

Types of Coverage That May Help — Even Without Phone Insurance

Even without a standalone phone insurance plan, you might have coverage you didn’t know about. Here are the most common sources:

1. Credit Card Purchase Protection

Many premium credit cards — including those from Chase, American Express, and Capital One — offer purchase protection that may cover theft within a set period (typically 90–120 days from purchase). Check your card’s benefits guide.

2. Homeowners or Renters Insurance

Providers like State Farm, Allstate, and Liberty Mutual often include personal property coverage under homeowners or renters insurance. A stolen phone may qualify as a covered loss, though a deductible typically applies and filing a claim could affect your premium.

3. Carrier Protection Plans (After the Fact)

Carriers like Verizon, AT&T, and T-Mobile offer protection plans, but these generally must be purchased at or shortly after device activation. You usually cannot add coverage after your phone is stolen.

4. Manufacturer Warranty

Warranties from Apple (AppleCare) or Samsung typically do not cover theft — they cover manufacturing defects and accidental damage only. This is an important distinction.

5. Third-Party Phone Insurance

Companies like Asurion, SquareTrade, and Upsie offer standalone phone insurance. Again, these must be purchased before a theft occurs, not after.

Coverage Comparison Table

| Coverage Type | Covers Theft? | Typical Cost | Best For |

|---|---|---|---|

| Standalone Phone Insurance (Asurion, SquareTrade) | Yes | $7–$20/month | High-value smartphone users |

| Carrier Protection Plan (Verizon, AT&T) | Yes | $9–$25/month | Those who want bundled coverage |

| Homeowners/Renters Insurance | Sometimes | Varies (deductible $500–$2,000) | Homeowners with high-value devices |

| Credit Card Purchase Protection | Sometimes | Free (card perk) | New purchases within benefit window |

| Manufacturer Warranty (AppleCare) | No | $3.99–$9.99/month | Accidental damage, not theft |

| No Insurance | No | $0/month now, $200–$1,200+ later | Not recommended for flagship devices |

Also Read: Does Insurance Cover a Cracked Screen? Full Guide

What Is Covered vs. What Is Not Covered

Understanding the boundaries of any coverage is critical. Based on typical policy terms, here’s what you can generally expect:

Typically Covered:

- Theft (with a police report, in most phone insurance plans)

- Loss in some premium plans

- Accidental damage (separate from theft coverage)

- Unauthorized usage charges (in some carrier plans)

Typically NOT Covered:

- Theft under manufacturer warranties

- Pre-existing damage before policy start

- Theft if the phone was left unattended in a public place (exclusion in some policies)

- Theft without a formal police report

- Phones not registered on the policy

- Claims made after the coverage window closes

Always read the fine print of your specific policy, as terms vary significantly between providers.

Costs, Deductibles, and What Replacement Actually Looks Like

If you do have coverage through homeowners insurance, expect a deductible of $500 to $2,000 or more — which may exceed the value of your phone. For a $900 iPhone, paying a $1,000 deductible makes filing a claim financially pointless.

Dedicated phone insurance plans typically carry deductibles of $29 to $299, depending on your device tier and provider. According to insurer guidelines from providers like Asurion, flagship phones (iPhone 15 Pro, Samsung S24 Ultra) usually fall into the highest deductible bracket.

If you have no insurance, you pay full replacement cost — either retail price, or a certified refurbished device price if you’re budget-conscious.

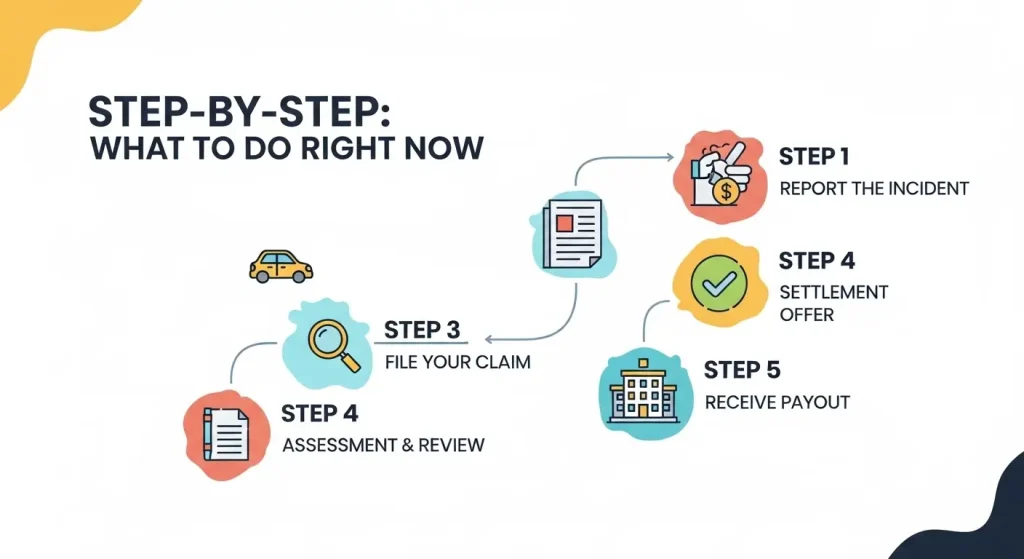

Step-by-Step: What to Do Right Now If Your Phone Was Stolen

Even without insurance, follow these steps immediately:

- File a Police Report — Do this as soon as possible. You’ll need the report number for any insurance claim now or in the future.

- Contact Your Carrier — Report the theft to your carrier (Verizon, AT&T, T-Mobile, etc.). They can suspend service, blacklist the device IMEI, and prevent unauthorized usage charges.

- Enable Remote Wipe — Use Find My iPhone (Apple) or Find My Device (Android) to remotely lock and wipe your device.

- Check Your Credit Card Benefits — Log in to your card portal or call the benefits line to ask about purchase protection or travel protection coverage.

- Contact Your Homeowners/Renters Insurer — Call providers like State Farm or Progressive to ask whether your personal property coverage applies.

- Document Everything — Keep receipts, the police report, purchase records, and any communication with your carrier.

- Purchase a Replacement — If no coverage applies, explore certified refurbished options through Apple, Samsung, or reputable third parties to reduce out-of-pocket costs.

Common Mistakes That Get Claims Denied

If you have any coverage that might apply, avoid these common errors:

- Not filing a police report — Most insurers require this for theft claims

- Waiting too long to report — Many policies have a 24–72 hour reporting window

- Not having proof of purchase — No receipt often means no claim

- Filing under the wrong policy type — Submitting a theft claim under a warranty voids the process

- Exaggerating the claim — Claiming a higher-value device than what was stolen is insurance fraud

- Missing the deductible math — Filing a claim that costs more in deductible than replacement value

- Not registering your device — Some plans require prior device registration

Is It Worth Getting Phone Insurance Going Forward? (The Financial Logic)

Let’s run a simple comparison:

- Phone cost: $999 (iPhone 15)

- Insurance cost: ~$13/month = $156/year

- Average claim deductible: ~$149

- Total out-of-pocket with insurance if stolen in Year 1: ~$305

- Total out-of-pocket without insurance: $999+

Over two years, you’d spend roughly $312 in premiums + $149 deductible = $461 — still saving over $500 compared to full replacement.

For mid-range phones under $400, the math is closer. For flagship devices over $800, phone insurance is generally worth it based on typical replacement costs and claim frequency.

Also Read: Best Health Insurance Plans USA 2026

Tips to Save Money on Phone Insurance (For Future Protection)

- Buy at activation — Carrier plans are cheapest and easiest to add at purchase time

- Compare third-party plans — Asurion, SquareTrade, and Upsie often undercut carrier prices

- Check your credit card first — You may already have free coverage you’re not using

- Bundle with renters insurance — Adding a scheduled personal property rider to a Geico or Allstate renters policy can be very cost-effective

- Choose the right deductible tier — Higher deductible = lower monthly premium; choose based on your financial cushion

- Don’t over-insure older phones — A 3-year-old mid-range device may not justify monthly premiums

FAQ: Phone Stolen No Insurance — Your Questions Answered

Does homeowners insurance cover a stolen phone? It depends on your policy. In most cases, homeowners and renters insurance cover personal property theft, including phones — but your deductible may be higher than the phone’s value. Check with your provider like State Farm or Liberty Mutual before filing.

Can I get phone insurance after my phone is stolen? No. Insurance must be purchased before a loss occurs. You cannot retroactively add coverage to claim a theft that has already happened.

What happens if someone uses my stolen phone to make purchases? Contact your carrier immediately to suspend service. Many carriers will investigate unauthorized usage charges. Credit card companies may also reverse fraudulent charges under their fraud protection policies.

How many claims can I file on phone insurance per year? Most phone insurance plans limit claims to 2 claims per 12-month period, according to standard insurer guidelines from providers like Asurion. Exceeding this limit typically results in claim denial.

Is filing a police report mandatory for a phone theft claim? In most cases, yes. Nearly all phone insurance plans and homeowners policies require an official police report as part of the theft claim documentation process.

Final Verdict + What You Should Do Next

If your phone was stolen and you have no insurance, the hard truth is that you’ll likely need to fund a replacement yourself — unless your credit card or homeowners policy offers indirect coverage worth exploring.

Going forward, the smartest move is to get protected before something happens. Whether you choose a carrier plan from Verizon or AT&T, a standalone policy from Asurion or SquareTrade, or a renters insurance rider from Progressive or Allstate, having coverage in place makes an enormous financial difference.

Don’t wait for the next loss to act. Review your current policies today, check your credit card benefits, and if you’re unprotected — get a phone insurance plan that fits your budget.

Your phone is valuable. Protect it like it is.